Current Mortgage Rates in the USA (2026)

Mortgage rates in the United States have softened slightly in early 2026 after a period of high borrowing costs during 2024 and 2025. The average 30-year fixed-rate mortgage is approximately 6.06%, while the 15-year fixed mortgage averages 5.38%, according to Freddie Mac. This moderation provides some relief for homebuyers and homeowners considering refinancing, although rates remain significantly higher than the ultra-low levels seen during the pandemic era.

How 30-Year and 15-Year Fixed Mortgages Affect Borrowers

The 30-year fixed mortgage remains the most widely used product in the U.S., offering predictable monthly payments over three decades. The 15-year fixed mortgage appeals to buyers who want to build home equity faster and pay less interest overall, though monthly payments are higher. Small differences in interest rates, even as little as 0.25%, can save hundreds of dollars per month on a typical mortgage, making careful comparison essential.

Government-Backed Loans Offer Competitive Options

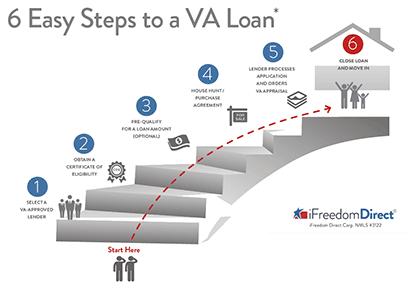

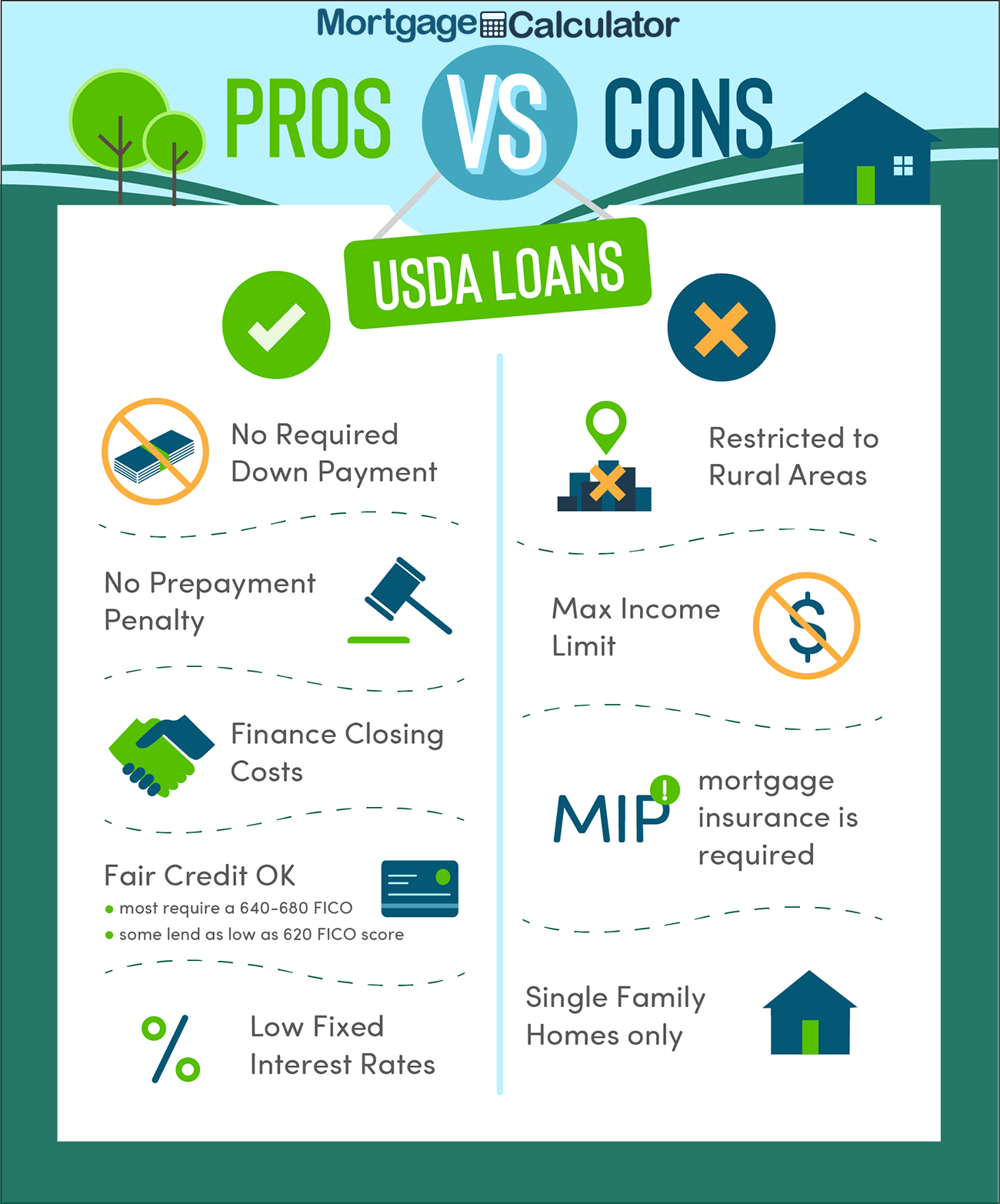

FHA, VA, and USDA loans continue to provide competitive advantages. FHA loans, designed for borrowers with lower credit scores or smaller down payments, often carry rates slightly below the national average for conventional mortgages, frequently under 6%. VA loans for eligible military members and veterans, and USDA loans for rural properties, offer low rates and minimal or zero down payments. These programs are particularly useful for first-time buyers or borrowers with limited savings.

Regional Differences in Mortgage Rates

Rates can vary across the United States depending on local housing markets, economic conditions, and lender policies. In the Northeast, mortgage rates tend to be slightly higher due to high housing demand and elevated property values. The Midwest and South generally offer more favorable rates, reflecting lower median home prices. In the West, rates can fluctuate due to urban housing markets and jumbo loan requirements. Buyers in competitive metropolitan areas may see slightly higher rates because lenders adjust pricing to account for market risk and property values.

Adjustable-Rate Mortgages as an Alternative

Adjustable-rate mortgages (ARMs) are another option for borrowers seeking lower initial rates. Popular products like 5/1, 7/1, and 10/1 ARMs offer a fixed interest rate for the first several years, followed by annual adjustments based on market benchmarks. These products can reduce early payments but carry the risk of higher costs if rates increase. ARMs are typically chosen by buyers who plan to sell or refinance before the adjustable period begins.

Factors Driving Current Mortgage Rates

Mortgage rates are influenced by several factors. The Federal Reserve’s monetary policy, inflation trends, and yields on 10-year Treasury securities are major determinants. Mortgage rates typically follow Treasury yields; when yields rise, rates increase, and when yields fall, rates decrease. Global economic developments, labor market data, and housing demand can also cause short-term fluctuations in rates.

Year-Over-Year Comparisons Show Improvement

Compared with early 2025, mortgage rates have declined. In January 2025, the 30-year fixed rate often exceeded 7%, while the 15-year fixed hovered around 6.25%. The easing in 2026 is largely due to Federal Reserve rate cuts in late 2025, slower inflation, and government purchases of mortgage-backed securities. Despite this improvement, rates remain well above the sub-4% levels seen during the pandemic, highlighting ongoing affordability challenges.

Implications for Homebuyers and Refinancers

Current mortgage rates affect monthly payments and long-term costs. Even modest reductions can increase a buyer’s purchasing power or reduce monthly obligations. Homeowners with higher-rate loans from 2024–2025 may find refinancing advantageous. Reducing a 6.5% mortgage to 6% on a $300,000 loan, for example, can save hundreds of dollars per month and tens of thousands over the life of the loan. Comparing multiple lenders, reviewing Loan Estimates, and considering all fees is critical to determining the most advantageous mortgage option.

Strategies for Navigating the 2026 Mortgage Market

First-time buyers and refinancing homeowners should monitor market trends, understand available loan products, and evaluate their personal financial profile. Government-backed programs remain particularly valuable for those with limited savings or credit challenges. Adjustable-rate options may provide short-term savings, but borrowers should carefully consider potential payment increases. Finally, working with mortgage professionals and using online comparison tools can ensure the best possible rates and terms.

Conclusion

Mortgage rates in the U.S. in 2026 are moderately lower than in 2025, with the 30-year fixed rate averaging just above 6% and the 15-year fixed rate around 5.38%. Government-backed loans such as FHA, VA, and USDA continue to offer competitive alternatives, while ARMs provide flexibility for certain borrowers. Regional variations and individual factors mean that careful comparison shopping is essential. Buyers and refinancers who stay informed, compare multiple lenders, and consider personal financial circumstances will be best positioned to secure favorable mortgage terms this year.